Significant Marketing Sector Transaction: Formation of the New Valve Group

M&A

M&A

Sell side

Valve Group has been created through a major restructuring involving Kaleva Group, Arvo Sijoitusosuuskunta and Valve. As part of the arrangement, Kaleva’s subsidiaries Kolmas Polvi Oy and Indieplace Oy join forces with Valve Branding and Advance B2B. The new group now brings together nearly 200 professionals with combined revenues of approximately €20 million, aiming to grow to €40 million by 2029.

The ownership of the new entity will be shared equally between management shareholders, Kaleva and Arvo. Both Kaleva and Arvo have also made substantial new investments to support the ambitious growth strategy.

Our team had the pleasure of acting as Kaleva Oy’s legal advisor in this transaction. The assignment was led by Partner Kirsi Karvonen, supported by Specialist Counsel Tiina Koivisto, Partner Kaija Pulkkinen, and M&A Manager Santeri Vaattovaara.

Kirsi Karvonen advises clients primarily on M&A and corporate transactions, including asset transfers, share exchanges, mergers, and demergers. Over the course of her career, she has been involved in hundreds of diverse transactions and corporate arrangements. Kirsi also has extensive experience in private equity investments and has advised numerous private equity funds.

The materials on the Eversheds Sutherland website are for general information purposes only and do not constitute legal advice. While reasonable care is taken to ensure accuracy, the materials may not reflect the most current legal developments. Eversheds Sutherland disclaims liability for actions taken based on the materials. Always consult a qualified lawyer for specific legal matters. To view the full disclaimer, see our Terms and Conditions or Disclaimer section in the footer.

We acted as legal and financial advisor to Aava Ohjelmistot Oy in the sale of its entire share capital to Jonas Software.

Aava Ohjelmistot Oy is a leading provider of ERP and MES solutions for the manufacturing and logistics sectors, built on a powerful in-house low-code platform. The company has earned a reputation as a trusted technology partner for small and medium-sized businesses seeking powerful, deeply tailored operational systems. At the centre of its offering is the Aava Platform, a proprietary low-code framework designed to build highly customised enterprise systems in a fraction of the time and cost of traditional ERP software. With a strong footprint in the metal industry and cargo vessel operations, Aava delivers business-critical solutions that help customers streamline complex processes, ensure operational control, and drive long-term efficiency.

Jonas Software operates over 180+ independently managed software brands worldwide, providing them with the strategic guidance and financial security required to be leaders in their respective markets. Jonas is an operating group of Constellation Software, Inc. (CSI), a public company listed on the Toronto Stock Exchange (CSU.TO). CSI has revenues of over $5 billion USD and over 30,000 employees across the globe.

Our team included Lead Partner Antti Husa, Associate Sanni Tirkkonen, Senior Associate Lavinia Husa, and M&A Manager Santeri Vaattovaara.

The materials on the Eversheds Sutherland website are for general information purposes only and do not constitute legal advice. While reasonable care is taken to ensure accuracy, the materials may not reflect the most current legal developments. Eversheds Sutherland disclaims liability for actions taken based on the materials. Always consult a qualified lawyer for specific legal matters. To view the full disclaimer, see our Terms and Conditions or Disclaimer section in the footer.

Another Strong Start to the Year for Eversheds Sutherland Finland’s M&A Advisory – Second Place in the Mergermarket Rankings

M&A

Buy side

M&A

Sell side

Following a strong 2024, Eversheds Sutherland Finland has once again achieved excellent results in M&A advisory this year. During H1/2025, we advised on 26 transactions, securing second place in Mergermarket’s Legal Advisors ranking in Finland by deal count.

“The early expectations for the Finnish transaction market in 2025 were more positive than what has actually been seen. According to our annual M&A Survey released in April, professional buyers found the market more attractive than before and also expected valuations to increase. Subsequent geopolitical events, not least the uncertainty regarding tariffs, however blurred the view again thereby slowing down the market.

On our desks, we see a lot of traction in particular in the TMT sector, with also healthcare and consumer sectors on the rise. Despite the decrease in interest rates, capital intensive businesses, such as construction and infrastructure, still need some time to really get going. The outlook for H2 is promising and we are confident of a steady deal flow in the coming months.

Our position as the runner up in deal count clearly underlines our ability to navigate the challenging and uncertain business environment. This is largely due to our broad international coverage enabling us to fluently carry out cross-border transactions, and our holistic approach combining legal and financial advisory, allowing us to deliver strategic commercial insight on valuation, deal structuring, and negotiation in addition to legal advice,” says Head of M&A , Partner Henrik Sandholm.

Our top rankings in Mergermarket reflect the strength of our expertise and our ability to support clients in demanding M&A projects.

Mergermarket is a leading provider of forward-looking intelligence and analysis on mergers and acquisitions.

Henrik Sandholm is the Head of Transaction Services team and a seasoned advisor specializing in both international and domestic corporate transactions, as well as transactions in the renewable energy and real estate sectors.

Expertise includes:

Mergers and acquisitions

Real estate

Energy and infrastructure

Commercial agreements

Corporate

International trade

The materials on the Eversheds Sutherland website are for general information purposes only and do not constitute legal advice. While reasonable care is taken to ensure accuracy, the materials may not reflect the most current legal developments. Eversheds Sutherland disclaims liability for actions taken based on the materials. Always consult a qualified lawyer for specific legal matters. To view the full disclaimer, see our Terms and Conditions or Disclaimer section in the footer.

The largest M&A event in Pirkanmaa will be held this year for the fifth time, once again bringing together experts and decision-makers from both the buy- and sell-side. The event serves as an excellent source of information and a platform for discussion for all stakeholders interested in corporate transactions.

The program features timely insights into the M&A market from top experts, business leaders, board professionals, and private equity investors. In addition, the spotlight will be on the role of employees in corporate transactions – how employee engagement and commitment influence the success and sustainable value of M&A.

Agenda

Opening Remarks

Keynote: M&A Trends in Autumn 2025 and the Eversheds Sutherland M&A Study 2025

Keynote: Kristiina Michelsson, CEO, OP Life Assurance

Panel – M&A Trends and Employee Engagement

Kristiina Michelsson, CEO, OP Life Assurance

Antti Liimatainen, COO, Eversheds Sutherland

Vilma Torstila, Investment Director, Bocap

Erik Alopaeus, Entrepreneur, M&A and Sales Expert

Antti Rauhala, CEO, Auroora Yhtiöt Plc

Networking Break

Keynote: Immo Salonen, CEO, Auntie Solutions Oy

Panel – The Changing World of Work

Immo Salonen, CEO, Auntie Solutions Oy

Pekka Vuorela, CEO, Go On Group Oy

Timo Jarmas, Partner, Eversheds Sutherland

Tuukka Ahoniemi, Professor of Working Life, Tampere University

Reetta Keränen, Young Board Member of the Year 2024

Closing Remarks and Networking Lunch

The event is free of charge. The language of the event is Finnish. Please registerby Wednesday, 27 August.

The event is organized in collaboration with Eversheds Sutherland, OP Pirkanmaa, Tampere Chamber of Commerce, and Business Tampere.

Secure your spot at the largest M&A event in Pirkanmaa.

The materials on the Eversheds Sutherland website are for general information purposes only and do not constitute legal advice. While reasonable care is taken to ensure accuracy, the materials may not reflect the most current legal developments. Eversheds Sutherland disclaims liability for actions taken based on the materials. Always consult a qualified lawyer for specific legal matters. To view the full disclaimer, see our Terms and Conditions or Disclaimer section in the footer.

Global luxury travel group Abercrombie & Kent has acquired Copenhagen-based Borealis DMC ApS, expanding its position as the world’s largest network of luxury destination management companies and establishing its foothold across the Nordic region.

Borealis DMC operates throughout Denmark, the Faroe Islands, Finland, Greenland, Iceland, Norway and Sweden, offering access to the region’s most sought-after experiences – from Northern Lights viewing to midnight sun adventures – while embracing a Nordic approach where luxury meets authenticity.

We acted as lead counsel for Abercrombie & Kent in the transaction. The deal carried strong Finnish connections through one of Borealis’ co-owners and businesses that stretch all over the Scandinavian and Nordic regions. Our role included full-scope legal due diligence, active participation in deal negotiations, general advisory related to legal and tax related questions, and reflecting these elements in the transaction documentation.

The acquisition forms part of Abercrombie & Kent’s global expansion, adding to recent investments in Mexico, Indonesia, Africa and South America, and further strengthening its reputation for combining cultural authenticity with high-end travel experiences.

Camille Drevillon, Chief Strategy Officer at Abercrombie & Kent Travel Group, commented: “Antti and his team were knowledgeable, proactive, and efficient, acting as an extension of the A&K team throughout this transaction. Their expertise and commitment were instrumental in bringing this acquisition to a successful close.“

The transaction was led by Partner Antti Husa supported by the team consisting of Counsel Elias Smouni, Senior Associate Lavinia Husa as well as Associates Sanni Tirkkonen and Josefina Lind.

The materials on the Eversheds Sutherland website are for general information purposes only and do not constitute legal advice. While reasonable care is taken to ensure accuracy, the materials may not reflect the most current legal developments. Eversheds Sutherland disclaims liability for actions taken based on the materials. Always consult a qualified lawyer for specific legal matters. To view the full disclaimer, see our Terms and Conditions or Disclaimer section in the footer.

M&A Market Showing Signs of Recovery — Commentary Featured in Kauppalehti

M&A

M&A

According to our recent market report, mergers and acquisitions activity is gradually picking up in Europe. Improved financing conditions and stronger corporate earnings are laying the groundwork for renewed deal interest, especially in core industrial sectors.

While we're seeing early signs of recovery, many strategic buyers remain cautious—particularly in cross-border transactions, says Henri Falck, M&A Director, Eversheds Sutherland Finland.

Kauppalehti recently featured our insights in their article on the evolving M&A environment, noting that although the pace of transactions is increasing, lingering macroeconomic and geopolitical uncertainties still influence timing and valuations.

Download our full report exploring the trends shaping the Nordic M&A landscape in 2025.

We hope the insights prove valuable. For further discussion or inquiries, don’t hesitate to get in touch.

Henri Falck specializes in commercial and strategic advisory for corporate and ownership transactions at Eversheds. He has extensive buy-side experience in private equity and has worked throughout his career with technology and software companies operating under the SaaS business model. At Eversheds, in addition to M&A transactions, Henri also advises clients on ownership arrangements related to growth financing.

The materials on the Eversheds Sutherland website are for general information purposes only and do not constitute legal advice. While reasonable care is taken to ensure accuracy, the materials may not reflect the most current legal developments. Eversheds Sutherland disclaims liability for actions taken based on the materials. Always consult a qualified lawyer for specific legal matters. To view the full disclaimer, see our Terms and Conditions or Disclaimer section in the footer.

In M&A transactions (share purchases), Net Working Capital (“NWC”) plays a pivotal role in determining the final purchase price. NWC and the associated purchase price adjustment mechanisms are essential components of most deals and can significantly influence the final equity valuation. When properly structured and effectively implemented, the NWC adjustments help protect the interests of both parties and contribute to a fair and balanced transaction outcome.

However, based on our experience, the concept of NWC is often misunderstood and sometimes misapplied, particularly in smaller transactions. It is crucial to recognize that determining NWC is not purely a technical exercise. The calculation and its outcome are influenced by a combination of market practices and business-specific characteristics, culminating in a negotiated agreement between parties.

Definition of Net Working Capital and Its Role in Purchase Price Mechanics

At its core, NWC typically consists of short-term assets specifically designated as working capital items (such as accounts receivable and inventory) minus short-term liabilities (such as accounts payable and accrued liabilities). The purpose is to evaluate the level of NWC typically required to operate the business on a normalized basis, often by reviewing average balances over a 12-month period.

In a professionally managed M&A process, the buyer typically proposes an initial estimate of the “Normalized NWC.” Based on this proposal, the buyer and seller, supported by their respective advisors, negotiate an agreed-upon working capital target, which is formally documented in the Share Purchase Agreement (“SPA”). At closing, the actual NWC is compared to this agreed target. If the actual NWC exceeds the target, the excess is added to the purchase price; if it falls short, the shortfall is deducted. This mechanism ensures that the purchase price accurately reflects the company’s true economic position at closing.

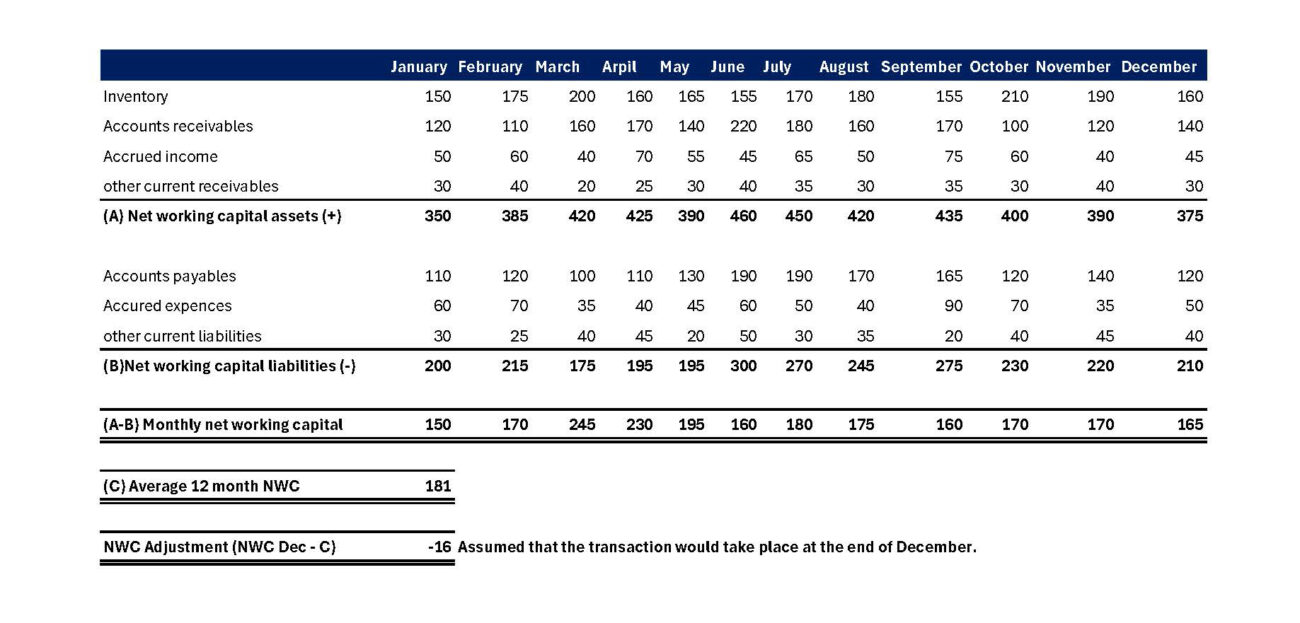

Simplified example to illustrate NWC calculation

According to market practice, it is expected that the target will be acquired including a “normal” level of NWC which is assumed to be included in the enterprise value (“EV”). This ensures that e.g., sufficient receivables and inventory exist relative to payables and other current liabilities, allowing the buyer to continue operations without the immediate need for additional capital injections. Conversely, should the NWC exceed the normalized level at closing, the surplus is typically for the seller’s benefit, as it represents additional tied working capital beyond what is required for the ongoing operations of the business. This situation might arise, for example, if the company makes a large sale of e.g. a product shortly before closing, resulting in a significant increase in accounts receivables. While the cash has not yet been received and booked to the bank account, the associated value of the deal beyond normal working capital need does not fully belong to the buyer.

When correctly implemented, the NWC adjustment mechanism protects both sides: the buyer secures the necessary resources to ensure operational continuity without immediate recapitalization and is safeguarded from risks such as aggressive receivable collection practices by the seller (aim to increase the cash in bank account, as it is added to EV, NWC adj. corrects this to buyers benefit), while the seller is protected against e.g., unfair buyer gains from unusually high levels of receivables outstanding at closing as described above.

A useful analogy is the purchasing of a car: If no other arrangement has been made, the buyer expects not only the price to include the vehicle but additionally the gas tank to be half full to drive away safely.

Practical Challenges in NWC Determination

While the principle of NWC appears straightforward, practical application often presents multiple challenges:

Which balance sheet items should be included in the calculation of NWC?

How to ensure that the calculation (inc. selected time period) reflects the most accurate level of the company’s true operational requirements (“Normalized NWC”)?

Have the monthly balance sheet items been properly accrued and fairly represent the business’s economic reality?

Have seasonal fluctuations or one-off anomalies been appropriately considered?

Although certain market practices exist, there is no universally applicable model for all NWC calculations. Typically, historical monthly average NWC levels are used as a benchmark, but other factors must also be considered:

Business Seasonality: For example, retail businesses experience significant working capital swings between seasons.

Exceptional Situations: Unusual payment terms, delivery delays, or inventory clearances may temporarily distort working capital levels.

Group Structures and Intra-Group Items: Intercompany receivables and liabilities must be separately analyzed and, where appropriate, eliminated from the calculation.

Experience shows that the best way to avoid post-closing disputes is to establish a clear, mutually understood calculation methodology early in the process, ideally documented already in the Letter of Intent (“LOI”). Doing so lays a strong foundation for smooth negotiations and minimizes the risk of late-stage transactional conflicts.

Conclusion

Although NWC represents just one component of an M&A transaction, its impact on the transaction’s outcome can be considerable. When properly structured, an NWC adjustment serves as an effective protection mechanism for both buyer and seller—but only if its details are carefully and expertly negotiated.

Therefore, we strongly advise all transaction parties to treat this topic with the seriousness it deserves and to engage experienced professionals early in the negotiation process.

Do you have questions about NWC in your upcoming transaction? Leave your contact details below and we’ll get in touch.

Santeri is an M&A Manager with extensive experience in corporate transactions. He has advised both buyers and sellers in numerous domestic and international deals, providing expert guidance throughout the transaction process. He holds a Master’s degree in Economics and Business Administration and is a Certified European Financial Analyst (CEFA).

Expertise includes:

Mergers and acquisitions

Business valuations

Financial modeling

The materials on the Eversheds Sutherland website are for general information purposes only and do not constitute legal advice. While reasonable care is taken to ensure accuracy, the materials may not reflect the most current legal developments. Eversheds Sutherland disclaims liability for actions taken based on the materials. Always consult a qualified lawyer for specific legal matters. To view the full disclaimer, see our Terms and Conditions or Disclaimer section in the footer.

The Merger of Meriaura Group Plc and Summa Defence Oy Has Been Completed

M&A

Buy side

M&A

The previously announced merger between Meriaura Group Plc and Summa Defence Oy, along with the associated arrangements, has now been finalized.

The transaction included, among other things, the following arrangements: • Acquisition of the entire share capital of Summa Defence Oy through a share exchange, with a purchase price of approximately EUR 188 million • Sale of Meriaura Oy shares to Meriaura Invest Oy for a purchase price of EUR 14.4 million • Directed acquisition of the company’s own shares from Meriaura Invest Oy • Change of company name to Summa Defence Oyj

Meriaura Group’s shares are listed on Nasdaq First North Growth Market Sweden and on Nasdaq First North Growth Market Finland. Trading of the new shares will commence on Wednesday, June 11, 2025.

Harri Tolppanen has taken care of hundreds of both domestic and cross-border mergers, acquisitions, investments and corporate transactions and their financing solutions, corporate restructurings, as well as related complex legal questions pertaining especially to company and contract law.

The materials on the Eversheds Sutherland website are for general information purposes only and do not constitute legal advice. While reasonable care is taken to ensure accuracy, the materials may not reflect the most current legal developments. Eversheds Sutherland disclaims liability for actions taken based on the materials. Always consult a qualified lawyer for specific legal matters. To view the full disclaimer, see our Terms and Conditions or Disclaimer section in the footer.

Kaleva Media Has Sold Kolmiokirja Oy to Dutch Keesing Media Group

M&A

M&A

Sell side

We acted as legal counsel to Kaleva Oy in the sale of the entire share capital of Kolmiokirja Oy to the Netherlands-based Keesing Media Group. We handled all legal aspects of the transaction.

Kolmiokirja is one of Finland’s leading publishers of puzzle magazines and popular weeklies. With this acquisition, Keesing strengthens its position in the Nordic market and continues its expansion across Europe.

The transaction was led by Partner Kirsi Karvonen, with help of Specialist Counsel Tiina Koivisto and Senior Legal Trainee Joona Eriksson.

Kirsi Karvonen advises clients primarily on M&A and corporate transactions, including asset transfers, share exchanges, mergers, and demergers. Over the course of her career, she has been involved in hundreds of diverse transactions and corporate arrangements. Kirsi also has extensive experience in private equity investments and has advised numerous private equity funds.

The materials on the Eversheds Sutherland website are for general information purposes only and do not constitute legal advice. While reasonable care is taken to ensure accuracy, the materials may not reflect the most current legal developments. Eversheds Sutherland disclaims liability for actions taken based on the materials. Always consult a qualified lawyer for specific legal matters. To view the full disclaimer, see our Terms and Conditions or Disclaimer section in the footer.

Ownership of Poppamies Oy Transferred to Saarioinen

M&A

M&A

Sell side

We advised the shareholders of Poppamies Oy in a transaction where Saarioinen Oy acquired the entire share capital of Poppamies Oy. As part of the transaction, the parties also agreed on a long-term lease of a property owned by the sellers, as well as a preliminary agreement on a future property sale.

Key shareholder employees committed to continuing their work with the company and contributing to its future development as part of the Saarioinen Group.

Our assignment included supporting the sellers during the legal due diligence process, drafting the share purchase agreement and related documents, and preparing the lease agreement and preliminary agreement concerning the property sale.

Poppamies Oy is a Finnish spice company best known for its chili and BBQ sauces.

Saarioinen is a Finnish family-owned company and a leading player in the ready-made meals industry.

The assignment was led by Partner Antti Husa, with support from Specialist Counsels Tiina Koivisto and Sinikka Turkki, and Senior Associate Lavinia Husa.

The materials on the Eversheds Sutherland website are for general information purposes only and do not constitute legal advice. While reasonable care is taken to ensure accuracy, the materials may not reflect the most current legal developments. Eversheds Sutherland disclaims liability for actions taken based on the materials. Always consult a qualified lawyer for specific legal matters. To view the full disclaimer, see our Terms and Conditions or Disclaimer section in the footer.

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.